•

We will lay out three key focus areas of launching a future-proof fintech platform in 2025 and a few nuggets for you to think about when you are ready to launch.

2025 is a perfect time to build a fintech lending platform. Inflation, interest rates will come down and many global conflicts will subside. Innovation in areas of A.I., energy, global communication is accelerating as we speak. We will enter into a decade of prosperity like we’ve never seen before.

Demand for credit will rise as well in the next 10 years and it’s not just within the United States, as Asia and the Global South develops, consumerism will spread and demand for access to credit from billions of people need to be addressed today.

Lending in the mobile and digital age has matured significantly. From access to liquidity to fund loans to conventional and unconventional data providers leveraging new methods of verifying and underwriting consumers. The ecosystem is ripe for financial services to leap into the market and create their vertical niche.

Banks and larger financial institutions are all gearing up to lending as well. Some banks have consolidated their offerings and are focusing on one of two products they know how to manage which gives fintechs more space to explore and innovate.

Now, here are 3 main points to consider when you launch a new future proof fintech lending company in 2025.

Access to liquidity:

The first thing to explore is your lending capital. No one will give you capital to lending without proof that you know what you are doing. Capital providers come in various forms, some are large pension funds, some are private equity funds and some are family office styled funds. Each type of these capital providers come with their own structure, e.g. what they want from you when they lend money to you to lend out to the masses.

However, all of them are looking at what you’ve done already and prove to them that you know how to manage a lending company and have advanced knowledge in credit risk management.

So how do you start without lending capital? Well, with your own money. That sounds crazy for some but it’s reality. You either use your savings or equity money you’ve raised from friends and family or venture capitalists. Most venture capitalists don't want you to use their money to lend, so you need to make sure that the use of their investment is well placed.

So, let’s say you amassed $250,000 to $500,000 dollars of lending capital from friends and family to lend. You need to think about how many loans you can produce and how long it will take for you to read the performance of these loans to give to your capital providers hoping that they will give you more money to lend.

If your loan amount is $500, you can lend to 500 to 1,000 loans. That’s a decent number of loans which you can draw some conclusions from the repayment performance. Now if these loans mature within 9 months, and you lend 100 to 200 loans per month, you might have to wait half a year to a year to let these loans seasons. While you wait, you might run out of money before the performance of the loans you issued come back. It’s not easy but it can be done.

A year has passed and you have a solid book of loans. The default rate is manageable and the interest you’ve charged on these loans covers the losses and some. You feel pretty good about yourself and walking these performances over to the capital providers.

These capital providers will typically lend you 70-80% of what you need. Meaning that if you want to lend out $1,000,000, they will give you $800,000 and you might have to come up with the additional $200,000 reserves to backstop and credit losses. Think about it as they provide the mortgage and you have to come up with the down payment on home.

There are other constraints of what the capital provider needs in order to return a profit, but we will not get into that in this article. The main point is that you have to show a book of loans with your own cash to show performance and more equity (cash) to raise the additional capital to lend from your capital providers.

Technology:

Whether you are well capitalized or bootstrapped your fintech lending outfit, you want to conserve as much cash as you can to operate your business and to keep your cash as part of the reserve requirements to your capital provider.

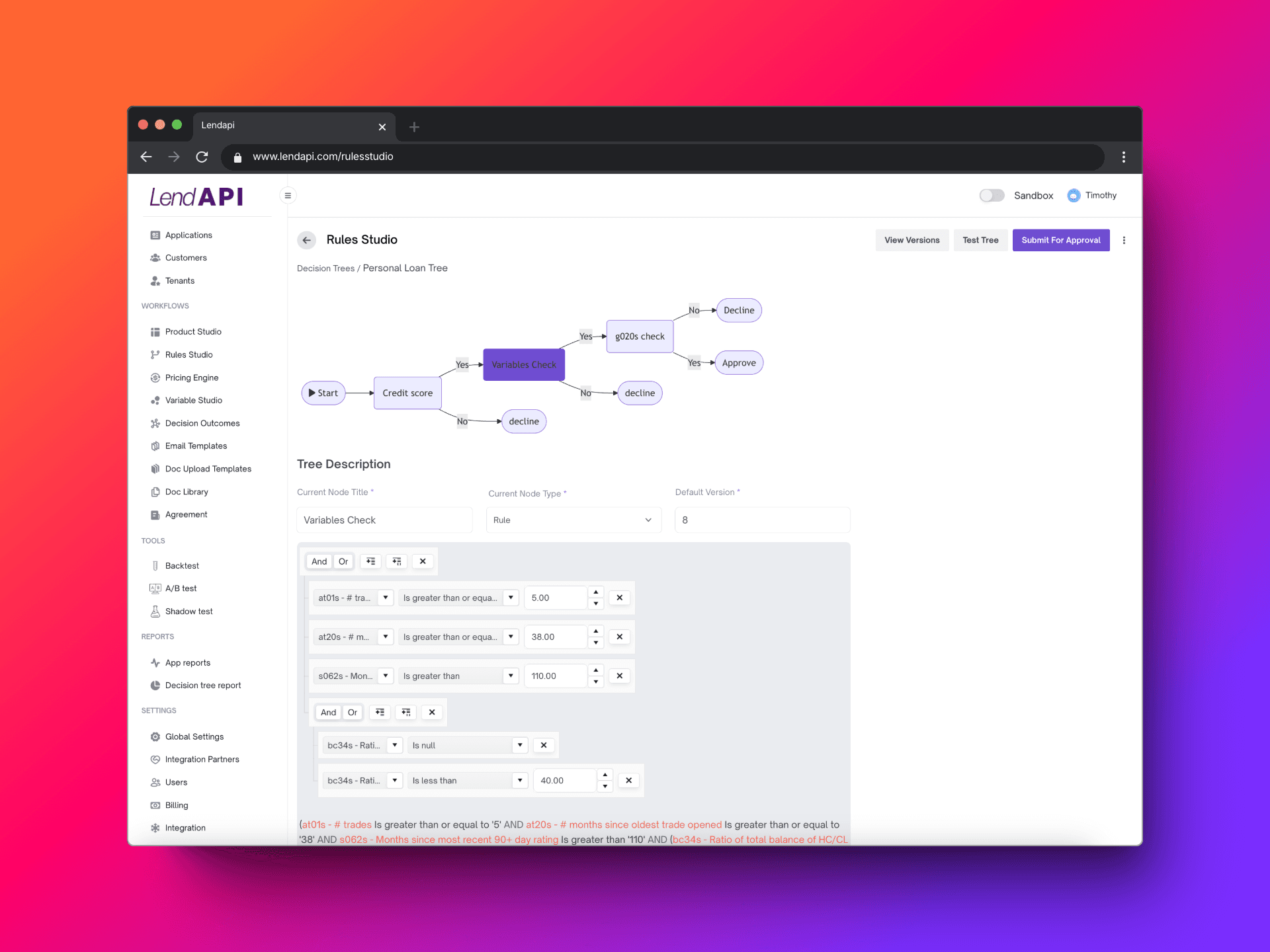

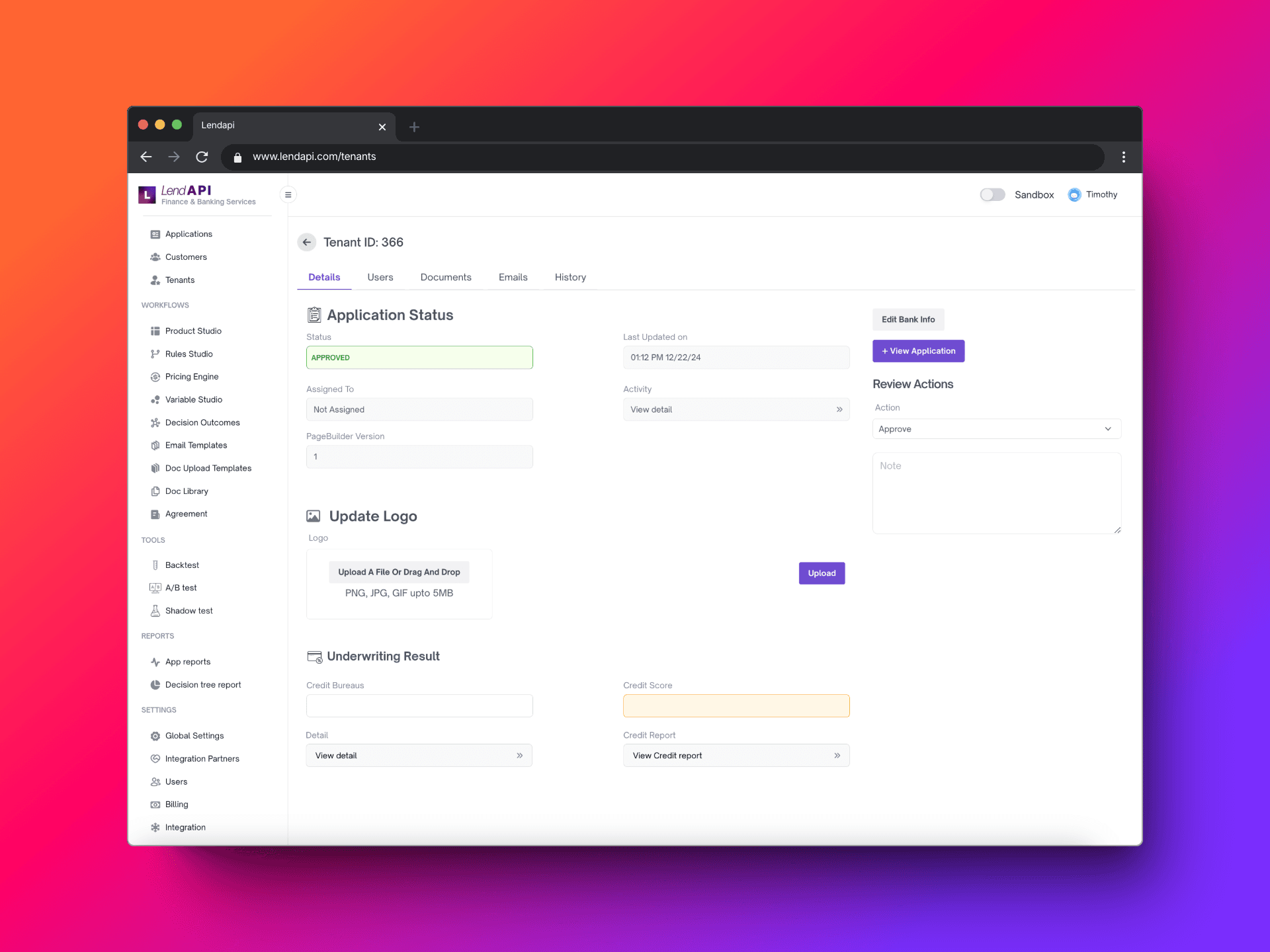

You want to leverage as much ready made technology to launch your business as soon as possible. LendAPI provides an entire platform for you to launch your customer application, customer portal, administrative portal, a decision engine and pricing engine that’s already plugged into most popular data providers. It’s a one stop shop to launch your entire outfit at a faction of the cost. And it’s ready to go on day 1.

The alternative is that you hire a team of engineers that could run up the cost into ten if not hundreds of thousands of dollars and wait a year or two for them to build something that already exists. And it may not have all the features you need and more money will be wasted to maintain and upgrade. We see a lot of fintech lenders go out of business not because of their portfolio performance but because their IT became unmanageable.

The analogy we like to use is that you wouldn’t need to build Google Docs or Microsoft Word to write an article like this today. You login, create an account and start writing. The competitive advantage is no longer in the tech layer, it is in your niche market.

Competitive Advantage.

Speaking of niche markets and your competitive advantage, what truly differentiates yourself from other lenders are three fold. “Cheap Leads”, “Cheap Money” and “Great Underwriting”.

“Cheap Leads” is when you have access to a specific market that no one or a few groups have. For example, if you are catering to and know how to access a specific demographic group (Hispanics or new to credit group). Or if you have access to professional groups such as doctors, schools, mechanics, you might be able to leverage the demographics or professional groups to provide leads to you. Why? For one, some of these markets are underserved so you don’t have to try as hard to get their attention. And with professional groups, if you are there to finance their clients, it's in their interest to get your name in front of their clients so they can gain a client as well.

LendAPI also provides professional group management functionalities where you can manage these groups with specific underwriting criteria and provide specific application forms for each of these groups. You can do all of this in real time.

“Cheap Money” is where you have done a great job on your initial portfolio that your capital provider will advance more than the traditional 70-80% of your capital needs. Let’s say that they like your niche, and you have demonstrated that your ability to control losses is best in class, they might advance you 85-90% of capital needed because they are confident in your execution. Potentially, they might even lower some of their ROI or fee requirements because they know that there's more certainty of a return with you than other people that they are funding. If you can leverage your money more than your competitors and maintain loan performance, you win every time.

To get to “Cheap Money” and make your capital providers happy, you must have “Great Underwriting”. Underwriting doesn’t mean access to a lot of data, it's the combination of industry knowledge and data science. If you are lucky to have a great credit risk manager, he/she can lay out some credit underwriting rules to start your portfolio. It might be conservative at first but you will learn from every loan and strive for a balance between approval and decline. Once you have 100 or 200 loans and a few months worth of payment cycles, the credit risk manager might use tools to build custom models whether they are logistic regression models, machine learning models or A.I. learning models.

The common problem that we see is that there’s no platform that can implement these models quickly and stamp out losses and increase ROI. LendAPI has one of the most robust decision engine and pricing engine for you to implement these models on your own. We also have staff members that can help you to implement these custom risk models to correct for your portfolio performance. LendAPI has processed tens of millions of transactions for large publicly traded fintechs that can easily handle the complexity and volume with your portfolio.

The alternative is that it takes many months to implement new strategies and your portfolio continue to suffer and you eventually lose the opportunity to demonstrate to your capital providers that you can manage your portfolio in an efficient and effective manner

If you want to talk about how we can help you launch your lending company, please contact us at info@lendapi.com. If you’ve finally decided to upgrade your decision engine and manage it yourself without dependencies, we would like to hear from you as well.

About LendAPI

LendAPI is a venture backed fintech builder launching any financial products in minutes. Follow us on Linkedin, X, YouTube, and check out our LendAPI Academy, LendAPI Podcast.