Mortgage Loans

What is a mortgage loan?

In the United States and some other countries with a well established capital markets, home ownership is made possible by mortgage loans. Banks and quasi-government agencies will provide capital to individuals, or even corporations to purchase homes, apartments, condos, commercial buildings.

Why is the government involved in making a mortgage loan?

In the United States, most of these mortgage loans are then sold from the mortgage banks to the government. Essentially, the government of the United States guarantees the performance to these loans given certain conditions.

The reason why the government is involved in homeownership is to encourage home ownership and let consumers own real estate and enjoy the appreciation of these assets as they mature. The other reason is to expand the US economy by lending money to those that want to own real estate and therefore the banks can collect interest on these loans.

Homeowners will also pay to secure homeowner insurance, pay property tax to the local establishment and all sorts of upkeep. These fees, interests, taxes and home improvement expenditures go back into the economy to pay for utilities such as schools, roads and other costs that go back to create jobs for the local economy.

How to obtain a mortgage?

Mortgage is one of the biggest expenditures an individual might ever consider in their lifetime. Depending on where you live in the United States, these mortgages range from tens of thousands of dollars to millions of dollars.

There are typically two types of mortgage loans. There’s a purchase mortgage loan, which means that the homeowner is buying a home. Typically these to-be homeowners have saved up a downpayment, (typically 1% to 20%) depending on the type of mortgage or program.

There is another type of mortgage called Refinance Mortgage, or “Refi”. This is where an existing mortgage holder wants to refinance their mortgage to lower their payment or take cash out from their equity to pay for larger life events such as tuitions, weddings etc.

The banks or a mortgage broker will either assign a mortgage bank to start collecting information from you or send you to an online application form to start the application process. Typically the entire process might take up to 30-45 days. There are various hurdles that the applicant needs to overcome to satisfy the banks or the governments underwriting criteria.

What are some of the key elements to be approved for a mortgage?

There are three key elements that go into a typical mortgage underwriting decisioning process.

Credit History

Credit history is perhaps one of the biggest portions and certainly one of the first items the mortgage underwriter reviews. Credit history can be obtained from any of the three major credit bureaus in the United States, Experian, Equifax and TransUnion.

Some mortgage banks will obtain credit history from all three credit bureaus to capture the entire picture of the applicant’s credit history. This is because not all creditors (such as credit card companies) report credit histories to all three credit bureaus. In order for the mortgage bank to understand your entire financial behavior, they often obtain credit reports from all three major credit bureaus.

The mortgage underwriters will look for any delinquencies, outstanding balances on existing loans and the length of your credit history. Most of the credit bureaus will summarize this information into an easy to understand three digit score called a credit score. It typically ranges from 300 to 900. The higher the score, the better your financial history and financial behavior.

Depending on the special program, you might need a 650+ credit score to qualify for a mortgage.

Income

Perhaps one of the most difficult items to verify is a person’s income. If you work for a company, your income is easily verifiable through a W2, pay stubs or a 1099 from. These forms are used as a receipt of your monthly or annual salary. Sometimes tax filing records and bank statements can also be used to verify your income and employment history.

There are many tools on LendAPI’s marketplace that can help mortgage bankers to obtain proof of income and employment. You can check them out at our Bank and Payroll Verification section of our marketplace. https://www.lendapi.com/marketplace/bank-and-payroll-verification

Small business owners, freelancers such as those that drive for Uber have a difficult time getting mortgages. Their income is irregular and sometimes personal income is mixed together with the company’s revenue even if the entrepreneur pays themselves through W2. The mortgage bankers will always need to chase the source of the money.

The underwriters are looking for stability of the income for those that don't have a job that pays W2 or a regular monthly income. A detailed analysis of these applicant’s bank account is needed. They sometimes have multiple income streams and it requires algorithms to lasso their income together to reflect their earning power.

Debt-to-Income Ratio

Whether the applicants have a high or low income level, this income steam is then weighted by the applicant's spending behavior. The mortgage underwriters is trying to determine whether the applicant has any additional income left over after each month’s debt obligation is paid.

If the applicant has a low debt to income ratio, for example, 30%, and the 70% free cash flow more than covers the new mortgage payment, then the applicant is well qualified. However if the applicant only has 30% free cash flow, any adverse event happening to this applicant’s life that requires emergency spending will put the mortgage payment in jeopardy.

Typically to get approved for a mortgage, the applicant has to have a certain level of income and the applicant's debt to income ratio should be less than 60-65% to be well qualified.

Debt-to-income ratio is typically calculated based on the verified income from an applicant’s W2 or tax records and collect all of the outstanding debt from the applicant’s credit report as well as other regular payments such as child support and alimony to get a true picture of the applicant’s free cash flow to take on additional debt, such as a mortgage.

Refi Mortgage Underwriting Criteria

When a current mortgage holder wants to refinance their mortgages, they will also fill out an application similar to the ones you would for a purchase mortgage. However the requirements for income and credit history are looked upon with less weight than the property itself.

For example, if the home value has risen and there’s a lot of equity value in the home, there’s less risk for the banks because the home has appreciated in value and therefore easier to pass refinance mortgage underwriting criteria. If the home equity value has appreciated a lot, there might even be a chance for the home owner to cash-out some of the equity on a refinance application. Essentially borrow against your home because the home equity value has risen.

Conversely, if the home didn’t appreciate in value or have lost value, the only outcome for a refinance would be to lower the monthly payments by stretching the payment period to another 15 or 30 years. This way, the monthly payments might be lowered to free up cash flow for home owners to have some additional buying power to purchase a car for example.

Mortgage Loan Originations Technology

Regardless of the type of mortgages you are offering, you will need a platform that’s connected to credit bureaus, income and employment verification as well as decision engines that can perform complex calculations.

If you want to quickly launch a mortgage application through your brokerage or your bank, take a look at LendAPI’s new mortgage application where you can private label this process and quickly launch your new mortgage originations outfit to capture marketing share when interest rates correct themselves in the coming years.

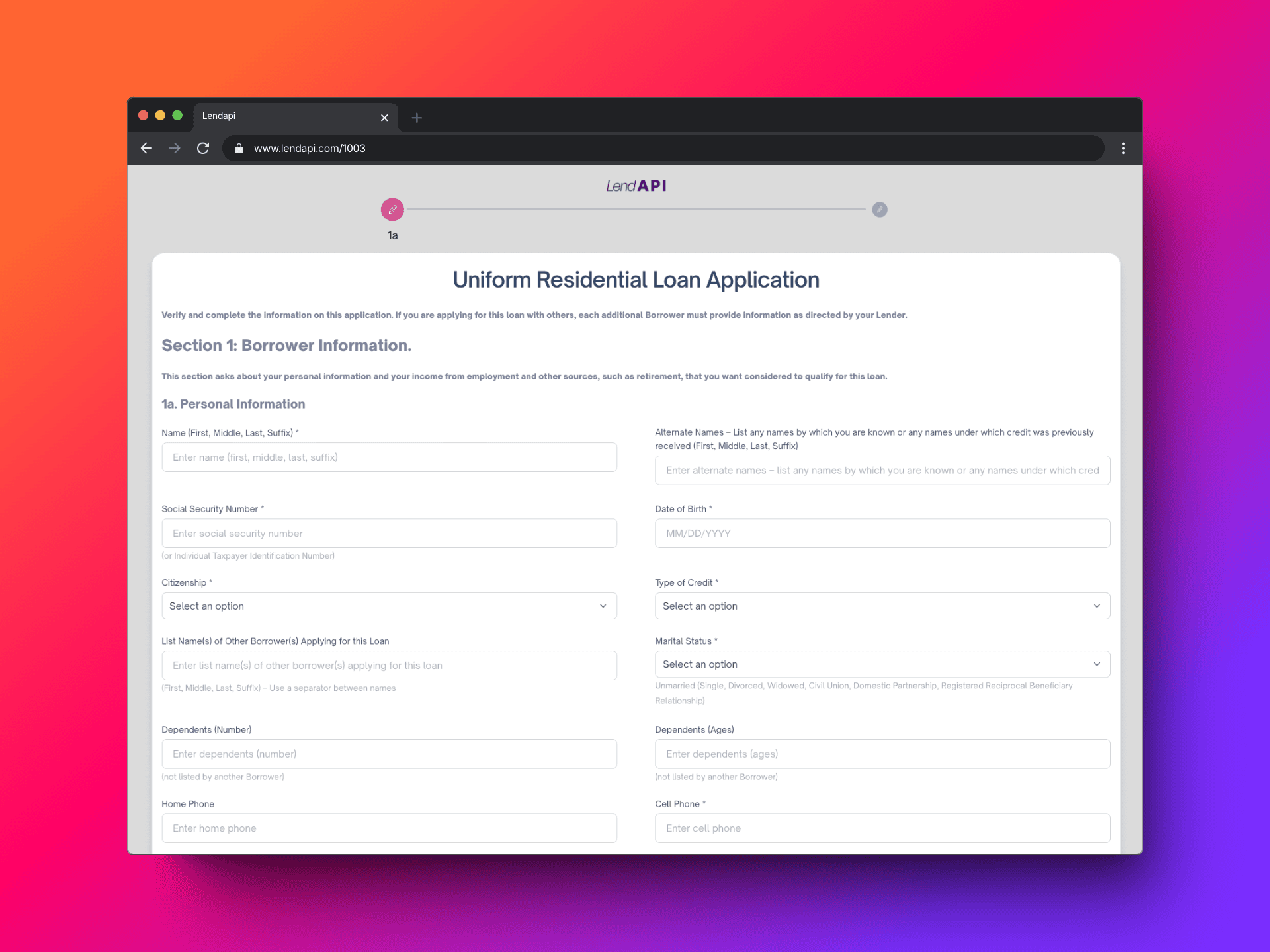

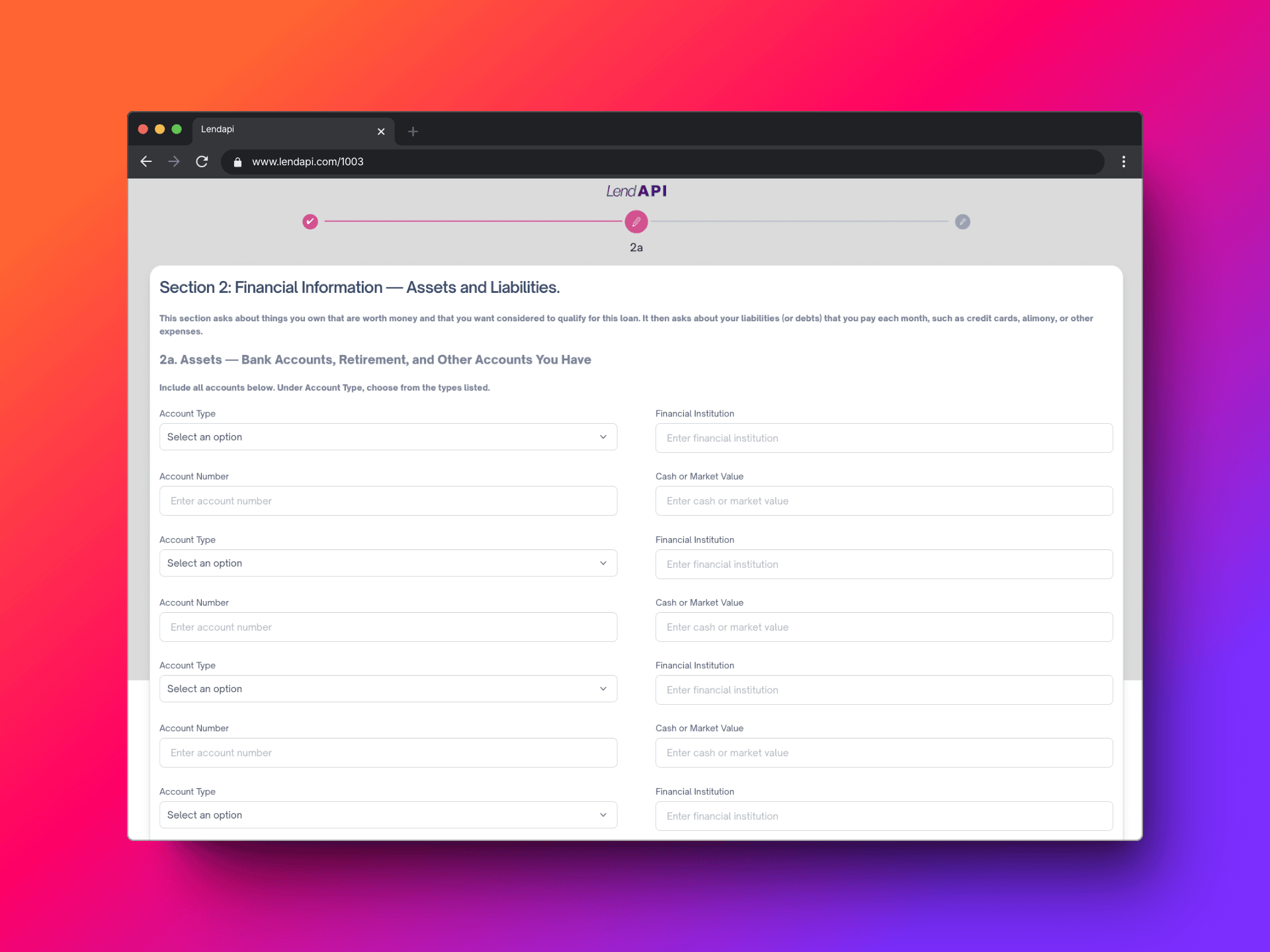

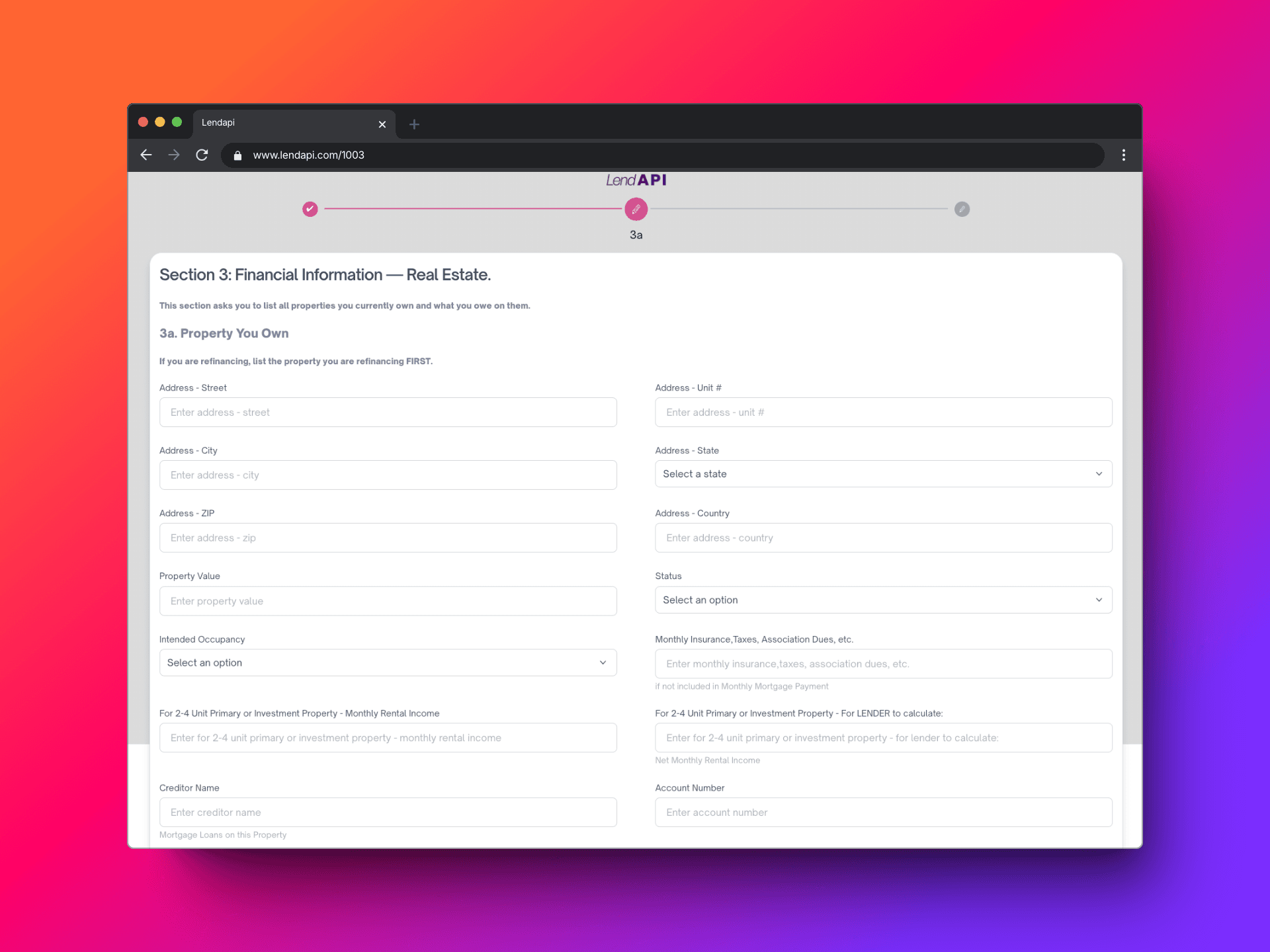

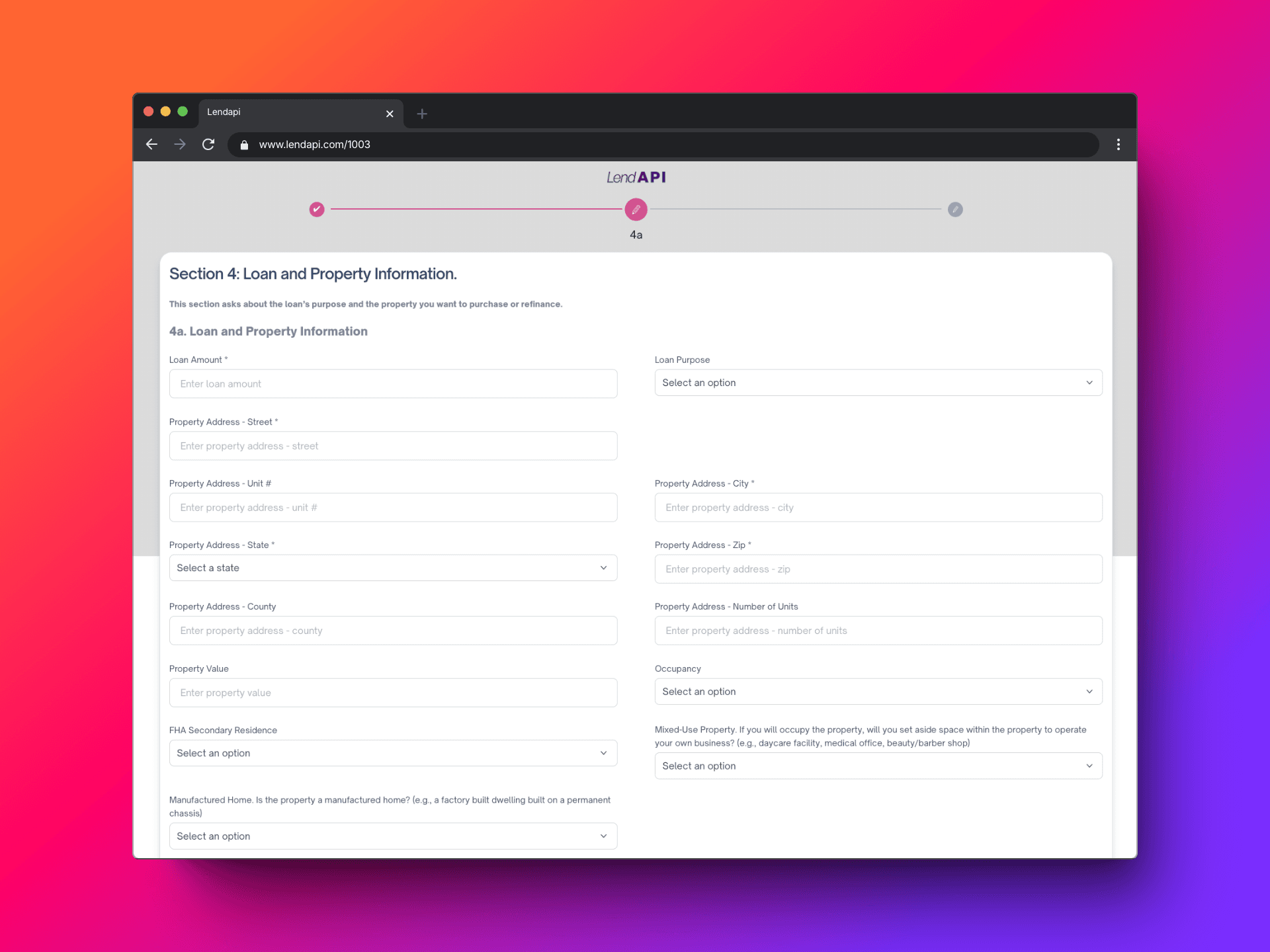

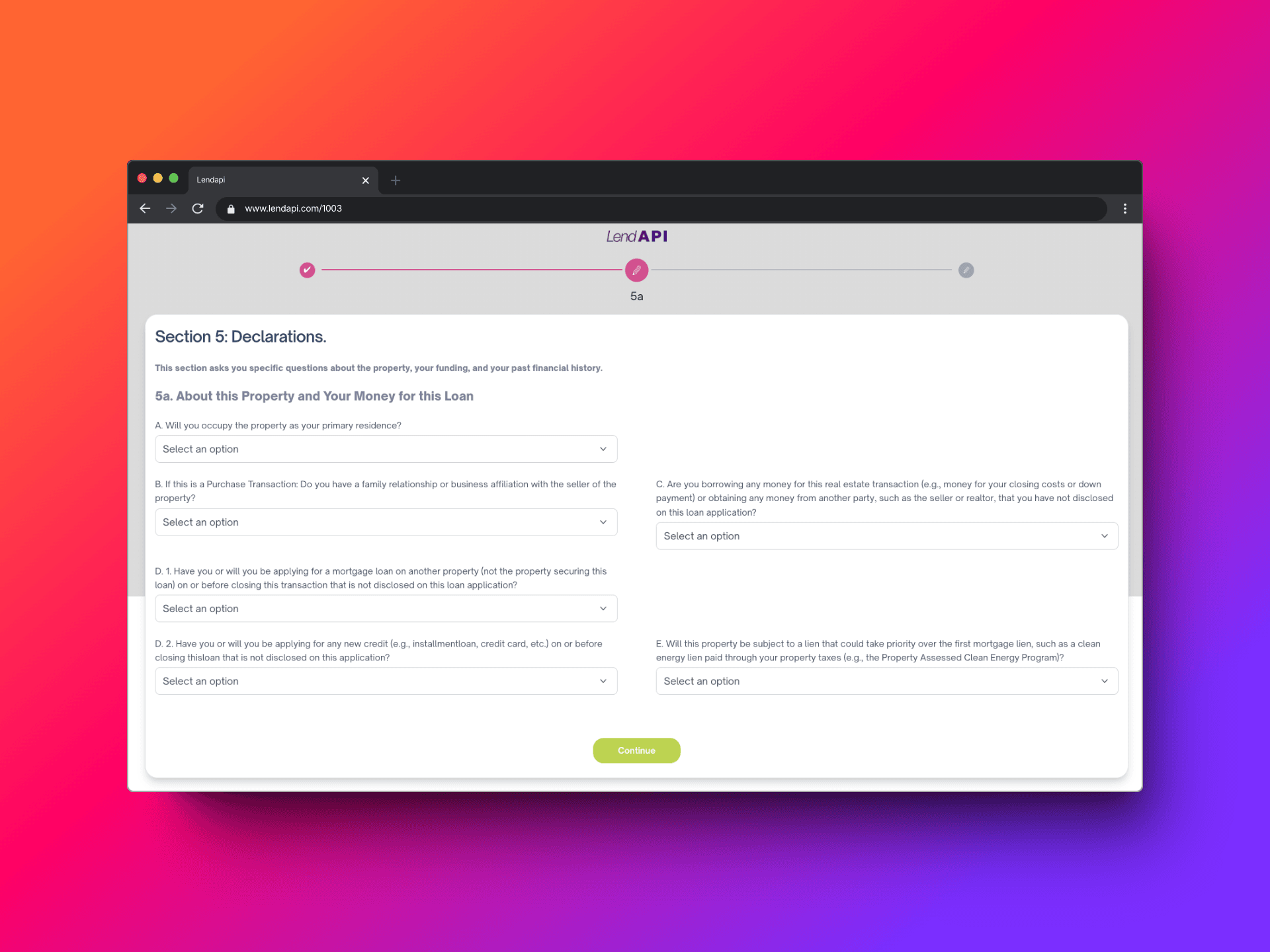

1003 Mortgage Application Examples from LendAPI

Here are a few screenshots of what to expect when you are using an out of the box mortgage application process with LendAPI. LendAPI’s new Mortgage Product also produced MISMO formatted file v3.4 and v3.6 which can be downloaded and uploaded to any mortgage bank that accepts this standard industry format.